Figure 1 - Configuration options for the Tenant Scorecard

Figure 1 - Configuration options for the Tenant Scorecard

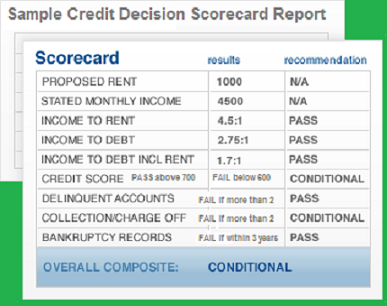

The configurable screening criteria for the Tenant Scorecard include credit scores, income to rent ratio, income to debt ratio, income to debt including rent ratio, delinquent accounts, collection/charge off accounts, and bankruptcy records (see Figure 1). A text box for entering the additional condition for conditionally approved applicants is also accessible. To enable a screening element for use in the Tenant Scorecard, place a check in the checkbox next to it. The pass/fail thresholds are prepopulated with average values, but should be modified according to the specific needs of the property.

For all criteria, numeric comparisons are made using strictly greater than and less than logic. If the data point is equal to the criterion, the condition will not be met. For example, if the Credit Scores element is set to fail below 580, and the credit score is equal to 580, the resulting recommendation will be conditional, not fail. In this example, a credit score of 579 or lower is necessary to generate a fail recommendation.

Conditional Approval – The Conditional Approval element specifies the additional requirement requested of the applicant when the scorecard recommendation is conditional. The additional requirement is generally a risk mitigating factor, such as an increased security deposit., or you may decide to ask for a copy of the applicant's bank statement(s) and/or pay stubs, tax return, etc. as factors to consider towards a conditional approval.

Conditional recommendations are the result of data being equal to or falling between the fail and the pass thresholds for a given scoring criterion.

If no conditional range is desired, the pass/fail thresholds should be set respectively to the desired threshold value and the desired threshold value minus one. For example, to eliminate the conditional range for the Credit Scores element with a fail threshold of 580, the Fail Below value should be set to 580 and the Approve Above value should be set to 579.

Credit Scores – The Credit Scores element compares the average of all credit scores returned in the credit report with the pass/fail thresholds for making a recommendation. The checkbox labeled “Include Manual Review for Results with No Score Records” allows two different ways to handle “No Score” results. If the checkbox is checked and the applicant has no credit score, a drop down menu of recommendation values is made available so that a manual review of the credit file can be made. For joint reports, if either or both of the applicants have no credit score, the drop down menu is made available (see Figure 2). If the checkbox is not checked, any “No Score” results are ignored and are not used in computing the average credit score.

Income to Rent Ratio – The Income to Rent Ratio compares the quotient of the stated income and the stated rent amount with the pass/fail thresholds for making a recommendation. The Income to Rent Ratio indicates how much income the applicant has in relation to the proposed rent. For example, an Income to Rent Ratio of 1.92 indicates the applicant earns just under two times the proposed rent amount.

Income to Debt Ratio – The Income to Debt Ratio compares the quotient of the stated income and the applicant’s monthly debt payment with the pass/fail thresholds for making a recommendation. The monthly debt payment is determined from the account history of the credit report. The Income to Debt Ratio indicates how much income the applicant has in relation to his or her monthly dept obligations. For example, an Income to Debt Ratio of 6.70 indicates that the applicant earns almost seven times his or her monthly debt payment.

Income to Debt Including Rent Ratio – The Income to Debt Including Rent Ratio compares the quotient of the stated income and the sum of the applicant’s monthly debt payments and the proposed rent payment with the pass/fail thresholds for making a recommendation. The monthly debt payment is determined from the account history of the credit report. The Income to Debt Including Rent Ratio indicates how much income the applicant has in relation to his or her monthly dept obligations combined with the proposed rent. The Income to Debt Ratio is calculated by dividing the income by the monthly debt payment. For example, an Income to Debt Ratio of 1.49 indicates that the applicant earns one and a half times his or her total monthly debt payments and the rent amount.

Delinquent Accounts – The Delinquent Accounts element compares the total number or percentage of qualifying delinquent tradelines with the pass/fail thresholds for making a recommendation. The account late payment history is determined from the credit report. The element can be configured to consider currently delinquent accounts; accounts with delinquencies in the past six, twelve, eighteen, or twenty-four months; or all reported delinquencies. The element can also be configured to ignore education/student loan tradelines as well as medical tradelines.

Accounts with late payments that fall outside the configured time frame or that are excluded by type are not included in the total number of delinquent tradelines, nor are they included in the total number of all tradelines used in computing delinquency percentages.

If both Delinquent accounts By Total and Delinquent accounts By Percentage are enabled, the qualifying tradeline data must pass both the total and the percentage thresholds for a pass recommendation. If the qualifying tradeline data fails either the total or percentage thresholds, a fail recommendation results. Similarly, if the qualifying tradeline data is in between the pass/fail thresholds for either the total or percentage thresholds, a conditional recommendations results.

Collection/Charge Off Accounts – The Collection/Charge Off Accounts element compares the total number or percentage of qualifying collection tradelines with the pass/fail thresholds for making a recommendation. The account collection or charge off status is determined from the credit report. The element can also be configured to ignore education/student loan tradelines as well as medical tradelines.

Accounts with a status of collection or charge off that are excluded by type are not included in the total number of tradelines, nor are they included in the total number of all tradelines used in computing the collection percentages.

If both Collection accounts By Total and Collection accounts By Percentage are enabled, the qualifying tradeline data must pass both the total and the percentage thresholds for a pass recommendation. If the qualifying tradeline data fails either the total or percentage thresholds, a fail recommendation results. Similarly, if the qualifying tradeline data is in between the pass/fail thresholds for either the total or percentage thresholds, a conditional recommendations results.

Bankruptcy Records – The Bankruptcy Records element considers bankruptcy records within the configured time frame. Bankruptcy records are determined from the public records section of the credit report. One or more qualifying bankruptcy records results in a fail recommendation.

Review Criminal Records Searches – If the Include Manual Review for Criminal Records Searches element is checked, a drop down menu of recommendation values may be made available to allow a manual review of the applicant’s criminal record search results. The drop down menu is only made available if the applicant’s file includes a County Criminal Records, InstaCriminal Statewide, InstaCriminal MultiState, InstaCriminal Research, or Sex Offender Records search (see figure 2).

Review Eviction Records Searches – If the Include Manual Review for Eviction Records Searches element is checked, a drop down menu of recommendation values may be made available to allow a manual review of the applicant’s eviction record search results. The drop down menu is only made available if the applicant’s file includes an Eviction Records or InstaEviction Records search.

Review Residential Verification – If the Include Manual Review for Residential Verification element is checked, a drop down menu of recommendation values may be made available to allow a manual review of the applicant’s residential verification. The drop down menu is only made available if the applicant’s file includes a Residential Verification.

Review Employment Verification – If the Include Manual Review for Employment Verification element is checked, a drop down menu of recommendation values may be made available to allow a manual review of the applicant’s employment verification. The drop down menu is only made available if the applicant’s file includes an Employment Verification.